- Gevelot (ALGEV) makes auto parts and pumps

- illiquid stock, trades 1 time/day (fixing)

- 97 m€ net cash on the balance sheet vs 131 m€ market cap (at 145 €/share). EV/2014 EBIT~5

- Management shows no sign of returning this excess cash to shareholders, a situation quite similar to GEA ; cash will be used for investment

- low valuation but the easy money has been made ?

1) The company

The company has 2 main activities :

- parts manufacturer for the automotive industry (Gevelot extrusion and Dold GmbH)

- pumps for industry, oil/gas, food processing (PCM pumps)

Manufacturing/extrusion

They have posted several videos on youtube about the production sites (plants in France and Germany). So it's industry, presses, cold forming, heat treatment, machining and lots of CAPEX.

Pumps (PCM)

Apparently their technological specialty is PCP pumps, used for instance in oil and gas. PCM was founded in the 1930's by the inventor of PCP pumps.

Carburators (Gurtner)

Division sold at a loss in 2014.

2) Why is it cheap ?

Gevelot owned a 45% stake in Kudu, a canadian pump supplier using this same PCP technology.

Gevelot bought the remaining 55 % from its main shareholder, and sold it right back in 2013 to Schlumberger. Kudu (45%) was valued at 10 m€ in 2012 Gevelot books and Kudu (100 %) was sold for 168 m€ to Schlumberger. Nate at oddball stocks made an article about it in 2014.

3) Where will the cash go ?

Not in the minority shareholders pocket for sure. No special dividend, no announcement for a major buyback program. There's not even an increase in the usual dividend. The company has a modest share buyback program running though.

The last annual report gives an indication about how the cash has/will be used :

- sale of Gurtner division (at a loss), which seems a good move to me (loss making division, not a great outlook on carburators...)

- investment (CAPEX) in Extrusion (13 m€), I'm not sure the return on this invested capital will be great given the historic profitability of this branch (see below)

- acquisition of AMIK Oilfield Equipement and Rentals (Canada). I'm not sure it's the best timing given the evolution in oil/gas prices but I'm not an expert and I don't know if the price paid is right.

The capital is entirely controlled by the family.

A notable shareholder is the fund "Stock picking France", with a deep-value style.

Another fund present at the capital is William Higgon's Independance et Expansion fund, that I've mentioned in some previous article.

However these funds have bought a long time ago and at a much lower price (years ago for the 1st one).

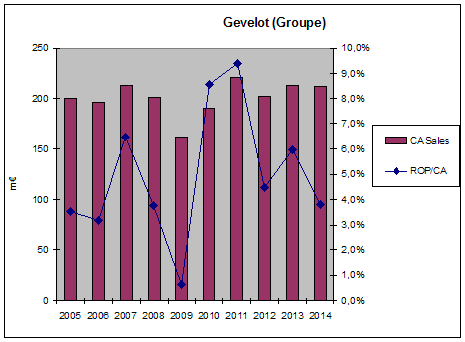

4) Financials

CA (Chiffre d'Affaires) = Sales

ROP/CA = EBIT margin

Breakdown between Extrusion and Pumps sectors

ROC = current operational result. MOP = current operational margin. Invest= investment

All figures (sales, results) are excluding intra-company transactions (more on that below).

The extrusion division is certainly not a "great" business: no competitive advantage, cyclical, heavy CAPEX, about 4-5% average (median value in the above table to be precise) operational margins. The outlook for the car industry seems recently better than the very difficult post 2008 years though.

The pump division has better margins (~10 %), less CAPEX requirements, but I've been unable to find the contribution of the oil/gas sector. Given the recent slump in oil prices, I wonder how to normalize earnings to account for the oil investment cycle.

5) Valuation

I've tried a sum of parts valuation, but one point that beats me is intra-company transactions (see table below). Just adding the estimated value of the extrusion and pumps branches without taking into accoung this internal transactions (-3 m€ in 2014) would lead to an overvaluation.

To get some idea, here's a very simplified DCF calculation, with conservative assumptions (no growth, average 4% margin, 12% cost of capital).

6) Conclusion

So yes Gevelot is cheap, but operates in a difficult business with no competitive advantage.

The lack of liquidity, and indifference to minority shareholders probably explains some part of the discount.

In any case it will take patience to see if the excess cash is used wisely and will produce results. Given the recent historical performance I doubt the return on this capital will equal its cost for a company like Gevelot.

Link to a very recent relevant article (Investing in bad businesses Damodaran).

Disclosure : long ALGEV

What do you think about DLSI ? they seem to be very cheap and some people say the industry will increase in the near future

RépondreSupprimerHello. I had a quick look at DSLI and its competitors Groupe Crit (CEN) and Synergie (SDG). They all trade at about the same EV/EBIT ratios ~7, cheap but not spectacularly cheap imho. I've added the stock to my watchylist though. Regards.

Supprimer